Generative AI is getting harder to understand, not easier. Elad Gil, an investor who called the frontier model oligopoly in 2021, before Llama and Mistral existed, now publishes a structured list of open questions across every layer of the AI stack. His prediction is holding: OpenAI, Google, Anthropic, Meta, and Mistral are the contenders, frontier training costs keep rising, and commodity model pricing keeps falling, with GPT-3.5-equivalent training now roughly 5x cheaper than two years ago.

The money tells the real story. Microsoft put $10B into OpenAI, Amazon and Google together put $7B into Anthropic, and Meta announced a $20B compute budget. Venture capital is a rounding error by comparison. Azure grew 6 percentage points from AI in Q2 2024 alone, an annualized revenue increase of $5 to $6 billion, roughly half of Microsoft's total OpenAI investment, returned every year. Cloud providers are not funding AI out of charity. They are funding their own revenue lines.

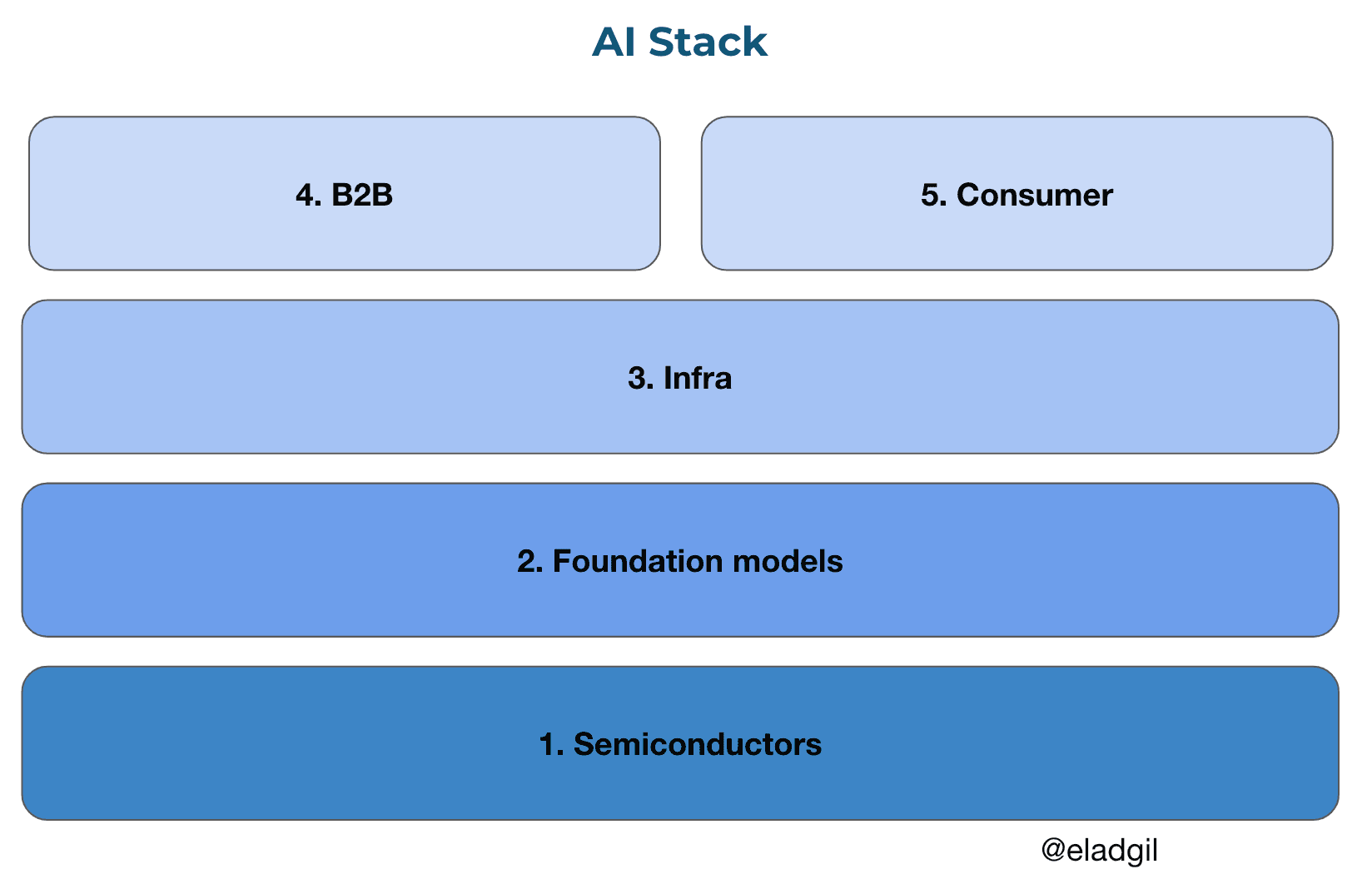

The value of this piece is not its conclusions. It is the questions Gil cannot answer: whether foundation model companies or cloud providers will capture the most value, whether open source models commoditize the entire stack, and where defensible margin actually lives at the application layer. These are the unresolved structural questions that will determine which companies matter in three years. Read the original for the full breakdown by stack layer.

[READ ORIGINAL →]